What is Exercise Tax? How to calculate it

Exercise tax incidence arises only when an employee is granted ESOPs, and they exercise these equity grants. Note that there is no tax implication during the vesting period.

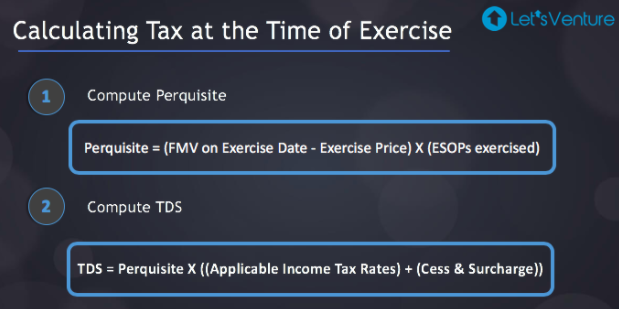

Upon exercise, if the Fair Market Value (FMV) of the share is more than the exercise price, then it becomes a gain for employees, and such a gain is treated as a ‘Perquisite’ in the hands of employees as per Section 17 of the Income Tax Act (1961). As a result, the employer (i.e., startup) is liable to deduct TDS on such a perquisite depending on the tax bracket in which the employee falls and deposits the same with the government before the 7th of the next month. This amount appears in the employee’s Form 16 and is included in his total salary.

Recently, in #Budget2020, FM Nirmala Sitharaman proposed the deferral of exercise tax to the time of sale of shares, 5 years, or when the employee quits the company, whichever is earlier. According to the proposal, the tax in such a scenario will now be required to be paid as follows:

- After the expiry of 5 years from the end of the relevant financial year in which shares are allotted, or

- From the date of the sale of such specified security or sweat equity share by the employee, or

- From the date on which the employee quits.

Such tax has to be deposited within 14 days of any of the above-mentioned events taking place.

Check out trica equity and manage your entire equity stack digitally!

Read this blog for a detailed insight on exercise tax (as per #Budget2020)

Click here for a blog on the tax outgo’s of ESOPs!

Disclaimer: This article has been prepared for general guidance on the subject matter and does not constitute professional advice. The matters described herein are general in nature and have not been evaluated based on applicable laws. You should not act upon the information contained in this note without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this note. LetsVenture Technologies Private Limited, its partners, employees, and agents accept no liability and disclaim all responsibility for the consequences of you or anyone else acting or refraining to act in reliance on the information contained in this publication or for any decision based on it. Without prior permission of LetsVenture Technologies Private Limited, this note may not be quoted in whole or in part or otherwise referred to any person or in any documents.

ESOP & CAP Table

Management simplified

Get started for free