ESOP Accounting for US GAAP

There is a lot of misconception around the accounting treatment and the requirement of valuation reports and disclosures for Employee Stock Options. Accounting treatment is different for various jurisdictions. In this blog, we will delve into the best practices for the US and explore various facets of US GAAP reporting that need to be kept in mind. This piece has been written in conjunction with Aranca, global research and analytics company. Let’s get started.

What are ESOPs?

Companies provide options (ESOPs) to employees to buy the company’s share at a fixed, predetermined price (strike price) on a certain date in the future. The strike price must be equal to the Fair Market Value of the company’s common stock at the time of grant to avoid penalty taxes under section 409A. This ESOP component is offered over and above the employee’s cash compensation to retain the best people.

This is a cost for the company (not in cash but in kind) and, as such, must be appropriately recorded in the books of account. The treatment of this cost or expense incurred by a company by issuing stock rewards is provided under FASB statement ASC 718, formerly 123 (R – Revised) code.

Accounting for ESOPs via US GAAP

Under ASC 718, the accounting treatment for stock rewards, measurement principles, and the valuation approach will depend on whether the awards are classified as equity or liability. The award may be classified as a liability under the following conditions:

- If the award is indexed to external factors such as price index or metrics of peer companies rather than company-specific factors such as share price, performance, or employee service condition or

- If it has a repurchase feature or requires the employer to pay the employee cash, the award should be classified as a liability.

While liability classifications might be rare and are most common in situations where we cannot easily conclude a fair market value for the award, they require due consideration to ensure compliance with reporting guidelines.

A simple case study to understand ESOP Accounting under US GAAP

We have structured our discussion in the industry-accepted chronology and explained the same with the help of an example. The below example will explain an ESOP journey for an equity-classified award of a company from the beginning using the Fair Value Approach. For ease of calculation, we have not assumed graded vesting for stock compensation expensing in the example below. Italics lines in between are the provision and the guiding principle, which one needs to follow and take care of.

Founders of Reckon Co are planning to introduce ESOPs in the compensation structure. With the help of their channel partners, Reckon could draft an ESOP scheme that was best suited to them.

They went ahead and got it approved by their board via a board resolution and by their shareholders via a special resolution on 21st December 2018. On 1st January 2019, Amy Winger, the Chief Business Officer, was granted 5,000 ESOPs and each option was convertible into one equity shares post completion of the vesting period of 4 years. Each year, 25% of Amy’s options (i.e., 1,250 options) will vest.

Now, to start with the ESOP accounting entries, we primarily need the following inputs:

- Exercise price: The strike price must be at least equal to the actual Fair Market Value (FMV) of the company’s share at the time of grant to avoid penalty taxes under section 409A. It is recommended that the FMV of the underlined share is based on a recently issued valuation report by an independent appraisal firm. With the help of independent appraisal firms such as Aranca, Reckon Co. establishes the FMV of common stock at $2.5 per share as of the grant date and thus sets the strike price of common stock options at $2.5.

- Fair Value of the option issued: With the help of independent appraisal firms such as Aranca that issues option valuation report, Reckon Co establishes the fair value of the option using the Black-Scholes Model of $2 per option as of the date of grant.

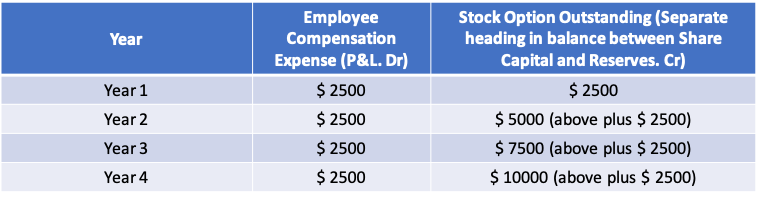

No accounting entries are required to be passed on the date of the grant. We need to have an option value in place, as discussed above. Accounting entries typically come into the picture on the completion of the first vesting. On 31st December 2019, Amy’s 1250 options will vest having an option value of $2 per option. We will be passing the below entry to record this expense:

Employee compensation of $2,500 will sit on the debit side of P&L, and the stock option outstanding will sit on the balance sheet as a separate heading between Share Capital and Reserve and Surplus.

Assuming Amy completes all four years of her vesting period, the same accounting entry will be passed on 31st December of Year 2, Year 3, and Year 4.

At the end of Year 4, the total of the Employee compensation expenses booked in the P&L would be $10,000 (i.e., 5000 option vested of $2 each), and also the Stock Options Outstanding A/c would show a total of $10,000 (i.e., 5000 option vested of $2 each).

Based on the ESOP scheme, Amy has the right to exercise the ESOP or not to exercise the ESOP. Accounting for both the possibilities will be as follows:

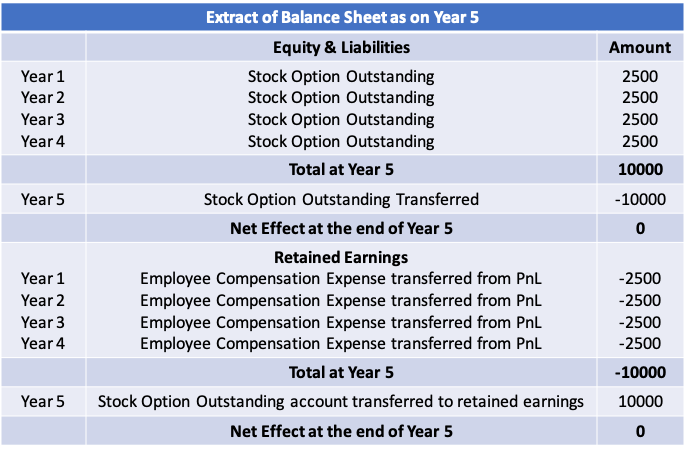

#1 | Amy does not exercise the ESOP within the exercise period

ASC 718 mentions that a pre-vesting forfeiture results in a reversal of compensation cost while a post-vesting cancellation would not. In the above example, all the options are vested. Hence, all 5,000 unexercised options represent post-vesting cancellations. Thus, as per the guidelines, the compensation cost of these 5,000 options will not be reversed in the profit and loss account (income statement). Instead, the balance standing to the credit of the ‘Stock Options Outstanding Account’ will be transferred to the ‘Retained Earnings’ account in the year the exercise period ends. In this case, to keep it easily understandable, we have assumed a 12 months exercise period. Thus, the transfer entry would be passed in Year 5.

At the end of Year 5, the balance sheet will look like this:

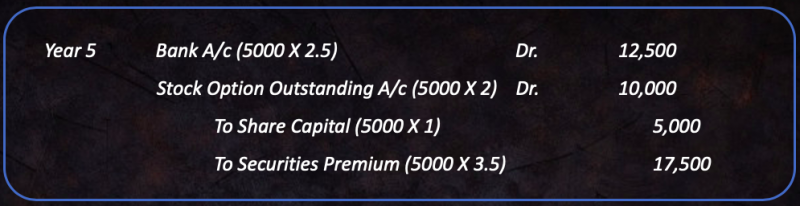

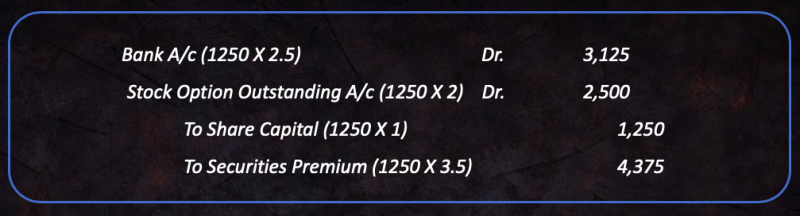

#2 | Amy exercises the ESOP within the exercise period (i.e., 12 months)

We can infer that Reckon Co. is liable to issue 5000 shares @ $2.5 per share (exercise price) to Amy if she exercises her right to convert the options into shares. Over a period of 4 years, Reckon Co. has booked expenses of $10,000 and a liability of $10,000. At the end of Year 5, all the options were exercised by Amy; therefore, Amy paid the exercise price, i.e., $12,500 (5000 X 2.5) to Reckon Co., and it issued 5000 shares to Amy.

The following entry is passed for the exercise and share issue.

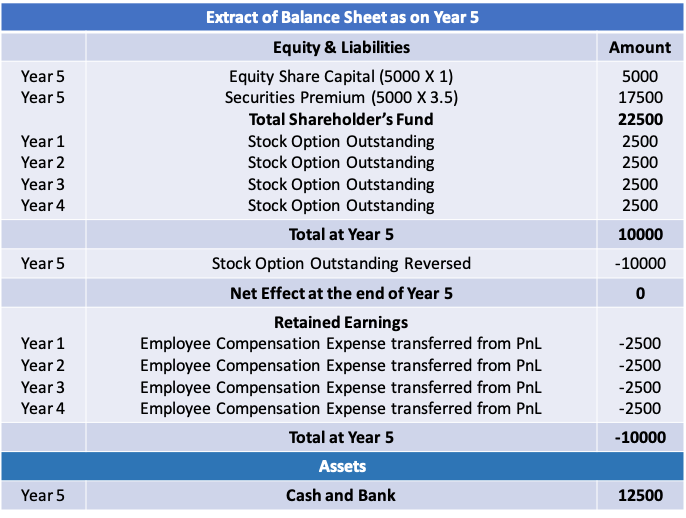

At the end of Year 5, the balance sheet will look like this:

Note:

#1 If the grant date is in between the financial year, then one can book the proportionate expenses as on 31st December based on the number of months passed using the below formula:

#2 If Amy left the organization after one year, post completion of 25% of her vesting, then the following treatment can be done:

Year 1:

Please note that 3,750 options represent pre-vesting forfeitures, and hence no compensation cost will be recorded with respect to such options. If recorded, it needs to be reversed in PNL.

If she has exercised 25% of her options:

If she does not exercise the options:

1,250 options represent post-vesting cancellations, and hence compensation cost with respect to such options should not be reversed in PNL. The following entry needs to be passed:

#3 On every grant date, Reckon Co. is liable to get an Open Valuation Report (OVR). As per the market practice and OVR, not older than six months is considered valid given there is no change in the terms and conditions of the two grants and no unusual event has happened in the company that can substantially hit the options valuation. Therefore, it is advisable to plan your granting of options in a 6 months period because, as per industry standards, the valuation report is valid for a maximum period of 6 months given.

About Aranca

Aranca is a global advisory firm with a wide array of financial and business advisory services. Aranca’s Financial Advisory Services include valuation opinions and corporate finance services for middle-market companies and start-ups. Within the Start-up community, Aranca has advised Clients on ESOP structuring and Option valuation for Tax and Financial Reporting purposes.

Disclaimer: This document is for informational use only, and certain accounting guidelines may have been updated/or no longer applicable. Nothing in this publication is intended to constitute legal, tax, or investment advice. The information contained herein has been obtained from professional accounting sources believed to be reliable, but Aranca does not warrant the accuracy of the information. Consult a financial, tax, or legal professional for specific information related to your own situation.

Click here for a blog on ESOP Accounting and Bookkeeping pertaining to Indian startups.

ESOP & CAP Table

Management simplified

Get started for free